The three most common reasons for setting up a fiscal risk control system are:

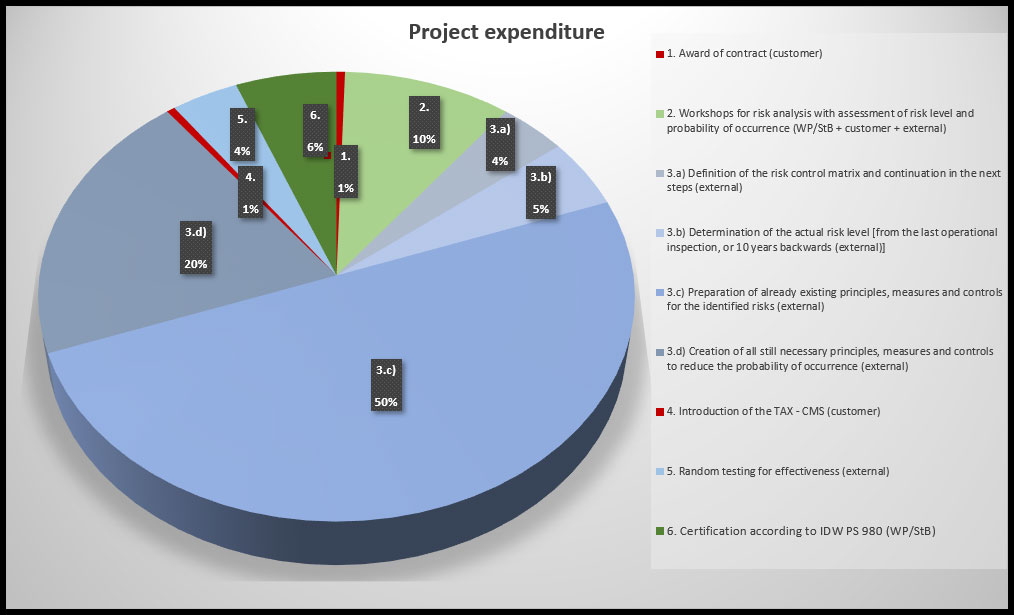

The results of the risk analysis workshops (2.) are used to create the risk control matrix (3.a). Coarser or finer grids can be selected for the risk level and probability of occurrence. The following example has five damage levels (0 = none, 1 = very low, 2 = low to medium, 3 = high, 4 = very high) whose amounts can be freely selected. For the probability of occurrence, 5 grids were also selected (0 = none, 1 = very low, 2 = low to medium, 3 = high, 4 = very high) whose percentages are also freely selectable.

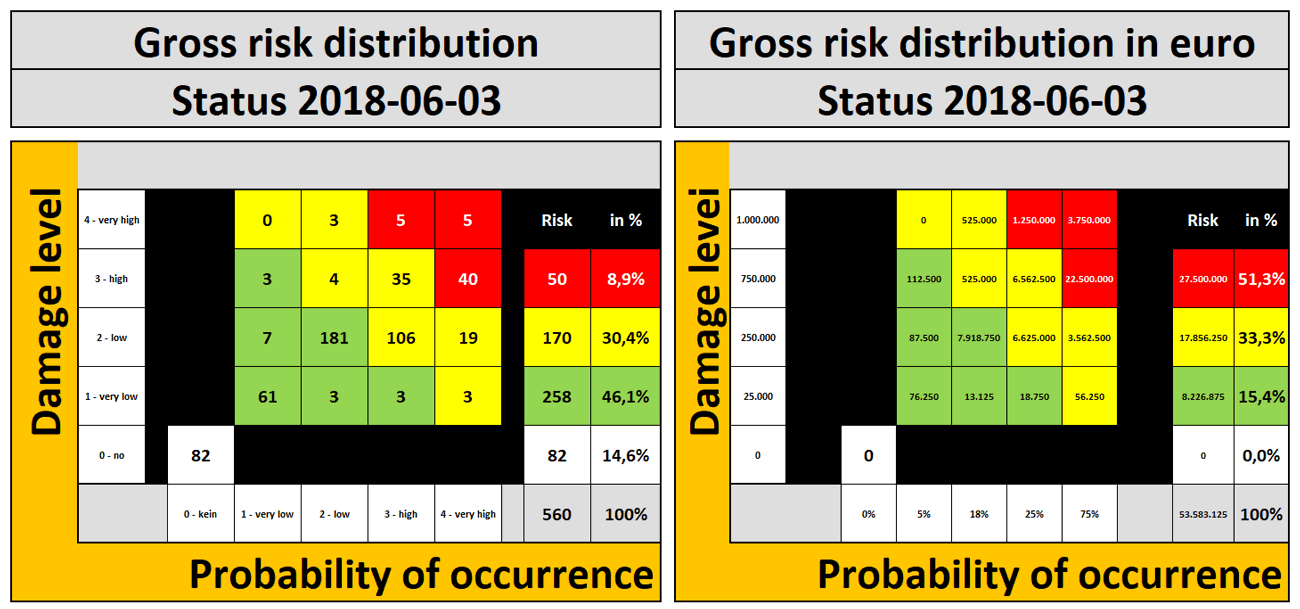

For many risks, the actual amounts of damage can and must be determined. In point 3.b) a correct calculation per risk is made.

Already existing risk minimization concepts are documented and checked in point 3.c).

The aim of a TAX-CMS project is to minimize the probability of risks occurring. For this purpose, necessary minimization activities are designed depending on the risk level (3.d).

Lettenstrasse 7, CH-6343 Rotkreuz

+41 41 790 52 42

info@fmc-gmbh.ch